Decisive Edge Newsletter | Land | April 2023

Newsletter Sponsors:

European sovereign industrial capability – decline and fall or a cooperative future?

While media attention has fallen on the lack of ammunition production capacity in the West due to the massive amount of artillery rounds being fired in Ukraine every day, this is masking a much wider problem in the land sector – in Europe at least!!

This is a wholesale decline in sovereign industrial capability, caused by the rapid downsizing of most armies which has not only lead to a significant round of corporate mergers and acquisitions but also contractors pulling out of the defence market altogether, as there is simply not enough business to sustain them in the long term.

In addition, the days are gone when many countries had well-established government-owned facilities capable of supplying everything from rifles to tanks for their own armies and even for export.

In France (GIAT) and the UK (Royal Ordnance), these have been privatised and in many cases key capabilities are lost as older facilities close down due to insufficient demand.

France now has just two main contractors in the land sector, Nexter (the former GIAT) and Arquus, with little overlap on product lines, and both firms cooperating on the latest key French Army wheeled armoured fighting vehicle (AFV) programmes.

Nexter has four production lines up and running for the Jaguar 6x6 recon vehicle, Griffon 6x6 armoured personnel carrier (APC), Serval 4x4 APC and of the CAESAR artillery system.

Above: The Jaguar 6x6 reconnaissance vehicle recently entered service with the French Army and has also been ordered by Belgium. (Photo: Arquus)

The Roanne site will also be responsible for upgrading the Leclerc MBT, where the hull was originally manufactured and mated with the turret built at Tarbes, a site which has now closed and is symptomatic of industrial decline.

Arquus was previously known as Renault Trucks Defense and at one time was up for sale. Its range includes products from the former ACMAT, Auverland and Panhard. Arquus is owned by Volvo group so can pull through commercial automotive technology into the defence sector.

In addition to Nexter and Arquus there are still key subcontractors in France including Thales (electronics and optronics) and Texelis (drive trains and suspension).

In Germany, the two main players left standing are Krauss-Maffei Wegmann (KMW) and Rheinmetall with the Boxer 8x8 Multi-Role Armoured Vehicle (MRAV) and Puma tracked IFV manufactured though a consortium.

Above: The Boxer MRAV is being adopted for an increasing number of specialised roles with this version fitted with a Rheinmetall 30mm turret. (Photo: Rheinmetall)

There were once two Leopard 2 MBT production lines in Germany but today the only one is at KMW in Munich, as they are now the design authority.

Rheinmetall produced a large number of Leopard 2s itself but today offers only upgrades as well as more specialised versions such as the Kodiak armoured engineer vehicle (AEV). More recently it developed the Lynx IFV as a private venture.

These French and German manufacturers are up against countries that have in the last 20 years or so become increasing active in the export market, such as South Korea and Turkey.

The latter country has two key AFV contractors which are in many respects complimentary, FNSS Savunma Sistemleri which is jointly owned by Nurol (51%) and BAE Systems (49%), and Otokar.

Above: The Cobra II is typical of the expanding range of vehicles developed by Otokar with this example fitted with a remote weapon station armed with a stabilised 12.7mm MG. (Photo: Otokar)

Both companies have done very well on the export market, in some cases even transferring technology to allow for local assembly or production.

More recently another Turkish company, BMC, has moved in on the AFV market. Otokar developed the country’s Altay MBT but the production contract was awarded to BMC, known mainly as a truck manufacturer.

BMC might be regarded as bucking the trend, and its emergence as a builder of tanks may have more to do with political expediencies than a forward-looking industrial strategy. Indeed, as the industrial base for the manufacture and assembly of platforms and weapons has decreased so have the huge number of subcontractors, large and small, as well as suppliers of raw materials.

The skills base is also vanishing – I recently talked to a major AFV manufacturer in Europe and he said: ‘There is a shortage of skilled welders. We have managed to get some but they were from one of our sub-contractors!’

For British Army Boxer production, RBSL sent welders to Germany to be trained and on their return to the UK they then trained additional workers for production of the Boxer Mission Module which is now under way.

There is also a shortage of steel armour as due to the increased demands created by the ongoing conflict in Ukraine.

Speaking to a major AFV contractor recently, he said: ‘We get our armoured steel from Sweden but we cannot order it in advance as we need a contract with the end user clearly defined.’ This means the company cannot stockpile armour in order to meet future requirements.

Also, the number of contractors who can manufacture artillery and tank gun barrels has declined and once the expertise for these is lost it is very difficult to get back.

In peacetime these barrels last many years due to the small number or rounds fired, but in a prolonged conflict artillery barrels can wear out when approaching 1,000 rounds fired at top charge.

‘There is a shortage of skilled welders. We have managed to get some but they were from one of our sub-contractors!’

Another hurdle for some European countries is end user certificates which means that some contractors cannot export to places like Saudi Arabia and, in one recent case reported to me, the Philippines.

And while China does not export AFVs to Europe, it has achieved major success in many parts of the world which, for Western contractors, are closed for political reasons such as human rights.

Against this darkening background, the future for European land contractors is though co-operation, which has proved to be very difficult in the past but must be the way ahead if what is left of the industrial base is to be retained.

Could a variant of M-SHORAD meet British Army air defence and antitank mission needs?

Moog Space and Defense Group is pitching its Reconfigurable Integrated-weapons Platform (RIwP) to meet a potential British Army requirement for a system capable of engaging both air and land targets.

The company already has a US Army contract for 144 units of which over 60 have now been delivered for integration aboard the Stryker 8x8 platform under the Maneuver Short-Range Air Defense (M-SHORAD) programme.

Above: A Stryker 8x8 in US Army Maneuver Short-Range Air Defense (M-SHORAD) configuration. A similar solution is being proposed to the British Army, although it would use a different base platform and weapons fit. (Photo: Moog Space and Defense)

The M-SHORAD configuration is armed with a pod of four Stinger surface-to-air missiles (SAMs) and a pair of Longbow Hellfire anti-tank guided weapons (ATGW), but can be configured for a dedicated air defence or anti-armour role.

The turret also has a stabilised L3Harris MX-GCS day/night sight and MM Hemispheric radar covering 360 degrees.

Close-in defence is provided by a stabilised XM914 dual-feed Chain Gun and 7.62mm co-axial machine gun (MG) with both reloaded under armour.

The baseline RIwP turret can be fitted with a range of direct and indirect fire weapons. Alternative ATGWs include TOW, Javelin and Brimstone plus laser-guided rockets while air defence options include Coyote and Starstreak missiles.

Moog is also currently developing a way to integrate directed energy weapons capable of addressing targets independently of the kinetic effectors.

For the UK the RIwP would carry the British Army’s choice of weapons, including (but not limited to) two missiles already deployed in service, the Thales Air Defence High Velocity Missile (HVM) for the air defence role and a pod of two MBDA Brimstone ATGWs.

Above: Moog’s Reconfigurable integrated Weapons Platform with a mock-up of four Thales HVMs on the left and two Brimstone antitank missiles on the right plus 30mm cannon and 7.62mm MG in the centre with stabilised sight alongside. (Photo: author)

The latter would meet the Battlegroup Organic Anti-Armour (BGOA) requirement which has four elements including Mounted Close Combat Overwatch (MCCO).

In addition to engaging conventional air targets RIwP could also counter the growing threat of UAVs with a 30mm cannon capable of firing proximity air-bursting munitions.

RIwP was originally developed by Moog as a self-funded venture to meet emerging customer requirements for a weapon platform capable of being quickly reconfigured by the user at depot level, to address evolving and new threats.

According to Richard Allen-Miles, international business development lead at Moog, RIwP achieves its objective ‘at Technology Readiness Level 8/9 whilst allowing 85% hardware commonality and a common user interface, thereby reducing the logistics and training requirement compared to other systems’.

Total weight of RIwP depends on weapon fit but fully loaded with gun, MG and dual missile pods can reach 1,500kg which still enables it to be fitted to a wide range of platforms, tracked and wheeled.

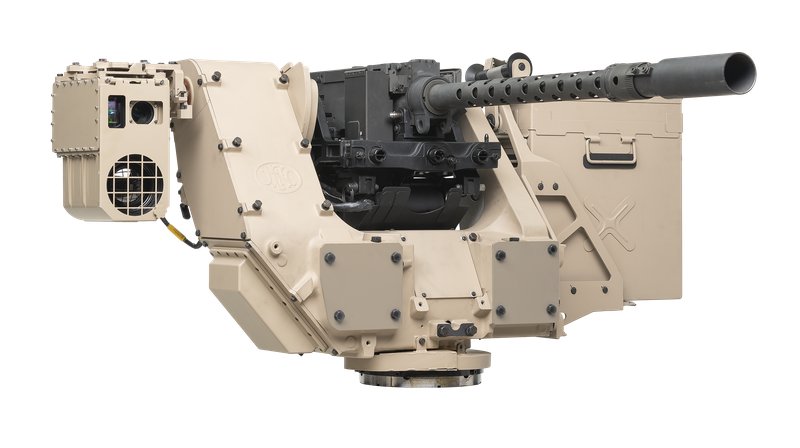

FN Herstal’s remote weapon station order book passes 2,000, but who is buying them?

FN Herstal has confirmed that sales of its deFNder remote weapon station (RWS) family have now passed over 2,000 units, setting the stage for production to continue well into the future.

The modular design of the deFNder allows it to be fitted with a wide range of weapons including 7.62mm and 12.7mm machine guns (MGs) and even a 40mm automatic grenade launcher (AGL).

Above: FN Herstal’s deFNder Medium remote weapon station armed with a 12.7 mm M3R machine gun with magazine on the left side and day/night sensor module on the right. (Photo: FN Herstal)

The company declines to give firm details of sales but Shephard’s sources state that until very recently most of these RWS have been for the highly competitive export market.

Domestic sales are not absent entirely as the Belgian Army will install FN’s RWS on its Nexter Griffon armoured personnel carrier (APC) which will form the Motorised Brigade of the Belgian Army Land Component. Some versions will have the deFNder Light and others deFNder Medium.

Belgium has also ordered the Nexter Jaguar reconnaissance vehicle but these will be fitted with the French Arquus Hornet RWS as this also fulfils the role of a coaxial MG.

Luxembourg has ordered 80 General Dynamics European Land Systems (GDELS) MOWAG Eagle V 4x4 to meet its requirement for a Command Liaison Reconnaissance Vehicle (CLRV) and these will be fitted with a deFNder Medium RWS armed with a 12.7mm MG. Prime contractor for this programme is Thales with FN Herstal and GDELS as sub-contractors.

The French Army will also fit an FN deFNder Medium to its upgraded Nexter Leclerc MBT and this will be armed with a 12.7mm M2HB MG.

Staying in France the Gendarmerie Nationale has awarded a contract to SOFRAM for a new 4x4 armoured vehicle called the Vehicule Polyvalent (Multi-Purpose Gendarmerie) and these will be fitted with the deFNder Light.

The Royal Netherlands Army will install deFNder Lights armed with a 7.62mm MG on some of its new Italian IDV Medium Tactical Vehicles (MTV) which will replace the currently deployed Mercedes-Benz G-Wagons.

These RWS have been ordered by IDV rather than being supplied as government-furnished equipment and the Italian company will be responsible for integrating these with the MTV.

It doesn’t end there. FN RWS are also installed on a number of unmanned ground vehicles with operators including Belgium, Estonia and the Netherlands and Milrem Robotics has demonstrated its THeMIS UGV-fitted deFNder Medium armed with a FN M2HB QCB.

Germany’s Puma IFV – all systems stop?

The start of 2023 has heralded a change of fortune for two of Europe’s biggest infantry fighting Vehicle (IFV) procurement programmes.

By Sam Hart, Defence Insight Analyst

Whilst the UK’s Ajax appears to have finally turned a corner of sorts in its development, Germany’s ongoing Puma programme has ground to a halt following the breakdown of an entire armoured company in December 2022.

In service since 2015, the Puma IFV has been Germany’s drip-fed replacement for the 1970s-vintage Marder IFV.

Above: As many as 200 of Germany’s Puma IFVs are believed to be classified as non-operational. (Photo: via author)

With final delivery achieved in 2021, the $4.72 billion original contract for 350 vehicles appeared successful, seeing two divisions at least partially equipped with the new IFV and the platform becoming the joint leading component with the Leopard 2 in Germany’s contribution to the NATO Very High Readiness Joint Task Force – Land (VJTF).

However, despite an estimated price tag of $8.1 million ranking the Puma as one of, if not the, most expensive IFVs in the world, reports surfaced as early as April 2022 highlighting that only 150 of the vehicles were operational, with large portions of the fleet mothballed, undergoing upgrades, or cannibalised to supply other Pumas.

Nicknamed ‘Pannenpanzer’ or ‘breakdown tank’ by elements of the German media, the Puma’s growing negative reputation was confirmed after a training exercise with the NATO VJTF involved a company of 18 Pumas all declared non-operational by the end.

This undoubtedly comes as a heavy blow to manufacturer Projekt System & Management (PSM), a joint venture between Krauss-Maffei Wegmann and Rheinmetall Landsysteme.

Although exact figures remain undisclosed, reports in 2022 indicated the German government had allocated funding to replace the remaining circa 210 Marder IFVs still held in inventory.

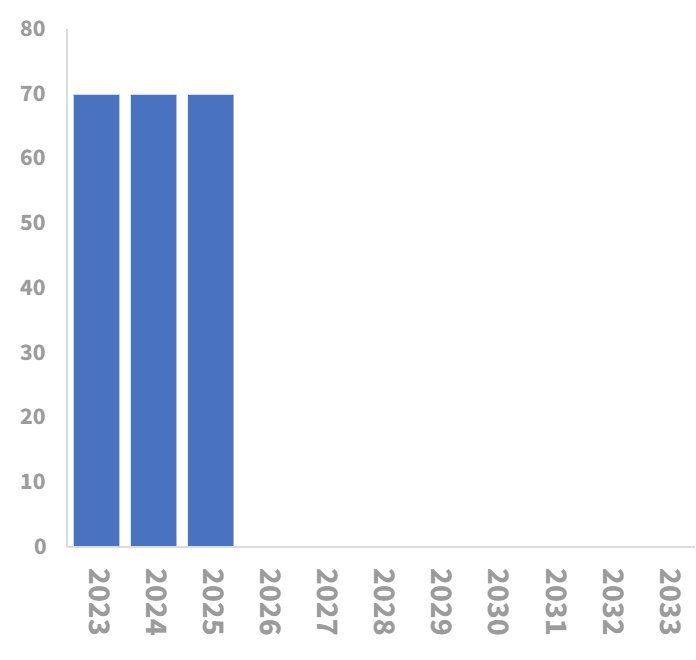

Estimated by Defence Insight to be worth at least $1.7 billion, this second Puma contract has since received the General Dynamics Ajax treatment as the German government publicly halts funding for future procurement until fixes are made.

|  |

Above: Germany’s projected annual expenditure and units funded for additional Puma IFVs over the next three years. The plan has now been put on hold until issues with the platform are resolved. (Source: Shephard Defence Insight)

Over a year after the announcement of a €100 billion ‘special fund’ for the German Armed Forces, the timing could not be worse for PSM.

Despite the money being split between the three arms of the German military, the Bundeswehr is expected to receive in the vicinity of €17 billion ($18.2 billion), with several big-ticket items rapidly rising in priority and popularity amongst German policymakers.

Already competing against additional Leopard 2s, Boxer IFVs and an estimated $1.3 billion 6x6 APC programme set to be awarded in 2023, the struggling Puma may well miss out on any additional orders in the wake of its ongoing defects and unreliability.

The timing is, unsurprisingly, also unfortunate for the German military, which recently donated 40 Marders to Ukraine and a further 40 to Greece from active Bundeswehr stocks.

As a result, the German military now finds itself in a vulnerable position with an IFV fleet half rendered ineffective before even leaving camp, paired with a now over 50-year-old platform that is under strength in numbers.

As IFVs continue to dominate European procurement discourse in the wake of their prevalence in Ukraine, the question is now how quickly the German Army and PSM will be able to return the Puma IFV to operational capability as NATO’s VJTF appears seemingly reliant on British and German Cold-War IFVs to form its spearhead.

Don't want to miss out on future Decisive Edge content? Make sure you are signed up to our email newsletters.